Reducing Everyday Business Risks with Liability Coverage

Key Takeaways

- Liability coverage protects businesses from financial losses arising from accidents, injuries, or property damage.

- A significant portion of businesses do not carry enough insurance, putting themselves at greater financial risk.

- Proactive safety protocols and workplace accountability play a critical role in reducing liability.

Table of Contents

- Understanding Liability Coverage

- Common Business Risks

- The Importance of Adequate Coverage

- Implementing Safety Protocols

- Fostering a Culture of Accountability

- Regular Policy Reviews

- Consulting with Insurance Professionals

- Conclusion

Running a business offers the thrill of growth and innovation, but every step forward exposes you to new risks. Customer injuries, property damage, or professional missteps can lead to lawsuits and unexpected costs, making it essential to manage these risks proactively. Implementing effective liability coverage is one way to shield your organization from potentially devastating financial fallout. To learn more about how liability insurance can be tailored to your specific business, it’s helpful to explore the basics and best practices of risk mitigation.

Many business owners underestimate the frequency and scope of everyday threats, leaving themselves vulnerable despite taking basic preventive measures. Without comprehensive protection, even a minor incident could strain resources or jeopardize operations. Liability insurance is not just a legal formality; it’s a strategic element in a company’s defense against claims of negligence, accidents, or property damage. Understanding which policies suit your industry and practices is fundamental for lasting stability and confidence.

While taking out an insurance policy forms the backbone of your protection plan, it’s just as vital to develop internal strategies that foster safe workplaces and personal responsibility among staff. Assigning clear roles regarding safety checks, encouraging open communication, and routinely evaluating workplace conditions all help prevent incidents before they occur. These practices, in combination with robust insurance, help minimize day-to-day business risks and foster an environment of trust for both customers and employees.

Industry reports consistently highlight a gap in business preparedness. A Hiscox study found that 77% of small businesses in the U.S. are underinsured, exposing themselves to unnecessary risk. Furthermore, cyber liability is rapidly growing as a concern, especially as companies continue to digitize their operations. According to a Gallagher survey, 72% of U.S. business owners are concerned that cyberattacks will affect their businesses over the next 12 months.

Understanding Liability Coverage

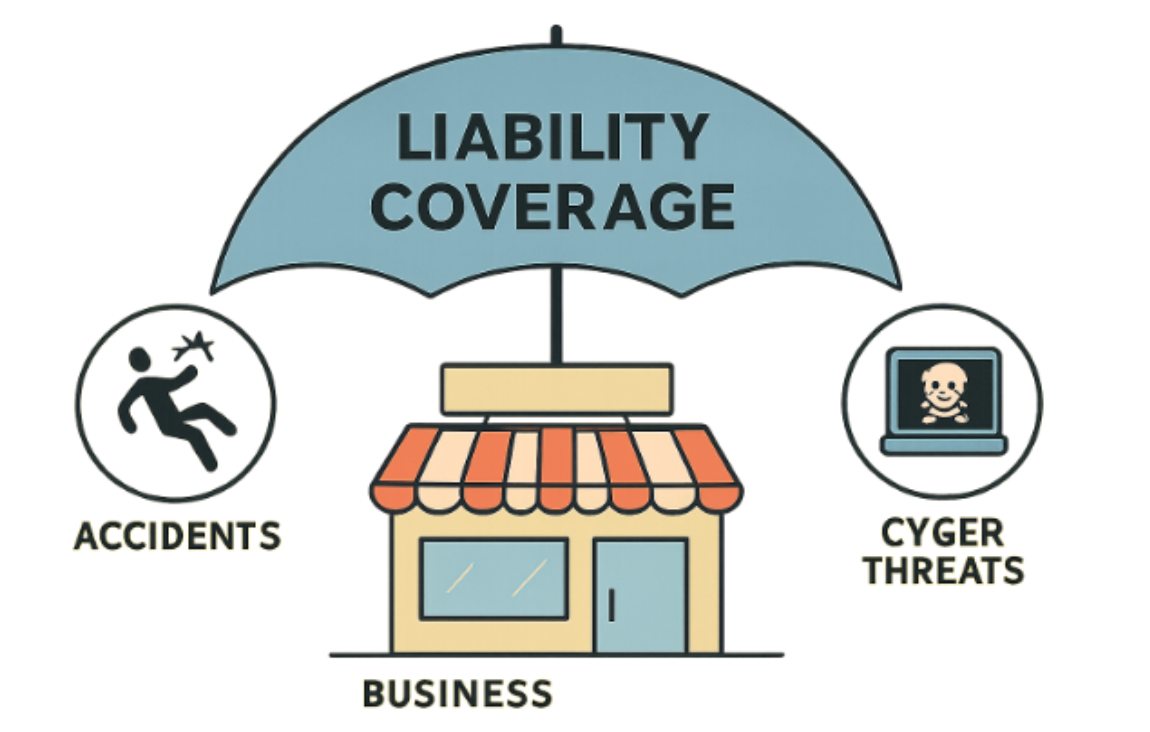

Liability insurance is the protective barrier that absorbs financial shocks from third-party claims. This may be from accidental injuries on your premises, damages resulting from your work or products, or professional errors that cause client loss. There are different policies for different business exposures: general liability covers bodily injury or property damage, professional liability handles claims stemming from mistakes or negligence in services, and product liability protects against claims regarding product defects.

For instance, most retailers and manufacturers need both general and product liability coverage, while consultants and service businesses typically opt for professional liability insurance. Choosing the right mix depends upon a thorough assessment of your daily operations, client interactions, and industry standards.

Common Business Risks

Everyday operations carry inherent dangers that could result in legal or financial problems for an unprepared business. Among the most common risks are:

- Customer Injuries: Slips, trips, and falls that occur on your property.

- Property Damage: Incidents that result in harm to a customer’s or third party’s possessions during business activities.

- Professional Errors: Mistakes made in the course of providing services that lead to financial losses for clients.

Modern risks also include data breaches and cyberattacks, especially as more small businesses move their operations online. According to a Gallagher survey, 72% of U.S. business owners are concerned that cyberattacks will affect their businesses over the next 12 months.

The Importance of Adequate Coverage

Underinsurance is a silent threat that can magnify the impact of an unfortunate event. According to industry data, a single slip-and-fall or professional error lawsuit often exceeds the basic coverage limits many small businesses carry. Hiscox reports that 77% of small enterprises in the U.S. are underinsured, leaving them at the mercy of enormous out-of-pocket expenses when unforeseen events happen.

Having sufficient protection in place increases a business’s resilience. It also builds credibility among clients and partners, who often check for proof of insurance before signing contracts or agreeing to collaborations. Adequate coverage forms the backbone of sustainable business planning.

Implementing Safety Protocols

While insurance mitigates the fallout from incidents, structured risk management practices help prevent those incidents in the first place. Some effective strategies include:

- Providing frequent and comprehensive workplace safety training for all staff.

- Utilizing clear signage and safety alerts in areas prone to accidents.

- Carrying out scheduled checks and routine maintenance on all equipment and facilities.

Written documentation of these efforts not only reduces risk but also provides proof of diligence if an insurance claim or lawsuit arises. Proactive attention to safety directly impacts a business’s liability profile and may even reduce premium costs over time.

Fostering a Culture of Accountability

A safe environment is rooted in shared responsibility. Encouraging employees to report concerns, rewarding vigilance, and hosting regular discussions about safety all contribute to a workplace where risks are addressed before they escalate.

- Host weekly or monthly safety meetings that encourage open dialogue.

- Maintain anonymous reporting channels so employees feel comfortable voicing issues.

- Recognize the contributions of staff who actively identify and reduce risk factors.

Accountability not only reduces liability risk but also demonstrates that leadership prioritizes the well-being of staff and customers, making it a valuable differentiator in the market.

Regular Policy Reviews

As your business grows and changes, so do your liabilities. Regular policy review is a critical habit. This ensures that your insurance coverage accurately reflects current realities, whether that means scaling up to accommodate staff growth, adding additional coverage for new products, or updating cyber risk provisions as you expand your online presence.

Review insurance annually or after significant business developments, such as acquiring new equipment, expanding physical locations, or entering new markets. This guarantees that you remain fully protected, no matter what changes.

Consulting with Insurance Professionals

No two businesses have identical risk profiles. Engaging qualified insurance professionals, brokers, agents, or legal advisors provides tailored insight and ensures you’re not overlooking critical gaps in coverage. They can help interpret industry trends, evaluate policy fine print, and advocate on your behalf with insurance companies if claims arise.

Regular consultations help to clarify your exposures and select the most effective insurance products, so that your business can navigate both everyday challenges and extraordinary disruptions with confidence.

Conclusion

Reducing daily business risk is a proactive journey. It combines adequate liability coverage with purposeful safety protocols and an organizational culture of accountability. Business owners who regularly assess their risks, keep their insurance up to date, and foster a safe and transparent environment are not just protecting against loss; they are investing in the ongoing success and reputation of their enterprise.